Margadh na meán

The Media Market

Maoiniú Stáit

Irish media might be described as a dual-funded model, financed by both commercial revenues and public income. However, the former has long accounted for the lion’s share of revenues even for public service media. In consequence the health of the media sector as a whole is closely tied to the state of the wider economy. During the era of the so-called “Celtic Tiger” (1995 – 2007) when the Irish economy grew at a previously unheard-of pace, advertising expenditure also ballooned and the revenues of advertising-funded media grew at an unprecedented rate, not least due to a property boom-driven explosion in accommodation-related advertising. However, when, almost overnight, the Irish economy collapsed in 2008, a process accelerated by over-leveraged banks and over-valued property, commercial media also suffered. Legacy media outlets in particular have never properly recovered, not least as online platforms came to dominate the advertising sector as a whole.

State Funding

State funding of media is largely concentrated on the two PSM, RTE and TG4. The main mechanism for collecting public funds is a television licence system which is levied on every household which contains television sets capable of broadcast reception. The licence fee is collected by the An Post (the Irish Post Office) which charges in the region of €12m per annum for this service. 7% of the licence fee is set aside and used to fund the Sound and Vision Scheme (see below) which is administered by the Media Commission. RTÉ receives the remaining licence revenue which, in 2021, amounted to €196m. TG4 receives the bulk of its revenues in the form of a direct exchequer grant amounting to €37m in 2021 with the rest of its revenues (€5m) coming from commercial sources.

License Fee

There has been extensive debate about the need to replace the television licence fee as a means of supporting the main public service broadcaster since 2009. With content now extensively distributed on the internet, access to public service media content is no longer reliant on television set ownership.Thus, an increasing number of Irish households have made statutory declarations that they no longer own a set and thus are not liable to pay a television licence. Evasion rates for those who are liable to pay the licence vary from 12% to 15% from year to year. This is considered high by European standards: according to the EBU, the average level of evasion in the EU in 2019 was 9.1%. Public disquiet relating to undisclosed payments to high profile presenters , news of which emerged in 2023, has driven evasion rates to even higher levels. Finally, the licence fee level is determined by the government of the day and Ministers appear to regard licence fee increases as politically damaging: the current licence fee of €160 has not changed since 2008.In 2017 a Parliamentary Committee recommended replacing the licence fee with a House Broadcasting Charge.

In 2021 the State-appointed Future of Media Commission recommended direct exchequer funding for both public service media (PSM) institutions. To date, neither recommendation has been accepted by Irish governments. In consequence, the state has been forced to plug the increasingly large holes in RTE’s finances with a sequence of “one-off” payments.

State Subsidies

State funding of private media is limited. Press subsidies have never been a feature of the Irish media landscape. After several decades of campaigning, the Irish newspaper industry succeeded in convincing the State to apply a zero-rate of VAT to newspapers from January 2023. The Future of Media Commission recommended that the state should fund some press content (e.g. court reporting) via a scheme to be administered by the Media Commission but this has yet to be established.

The Sound and Vision Scheme administered by the Media Commission is available to any radio or television production company based on the island of Ireland (including Northern Ireland). Worth between €15m and €20m per annum, the scheme supports the production of public service content which may be screened on any broadcaster in Ireland, be they PSM, commercial or community-based.

The State also funds film, television and animation production via Screen Ireland (2021 Budget: €38m) and the Section 481 Tax Mechanism which was worth approximately €98m in 2021. Screen Ireland and Section 481 mainly fund drama production but also support a significant amount of documentary output.

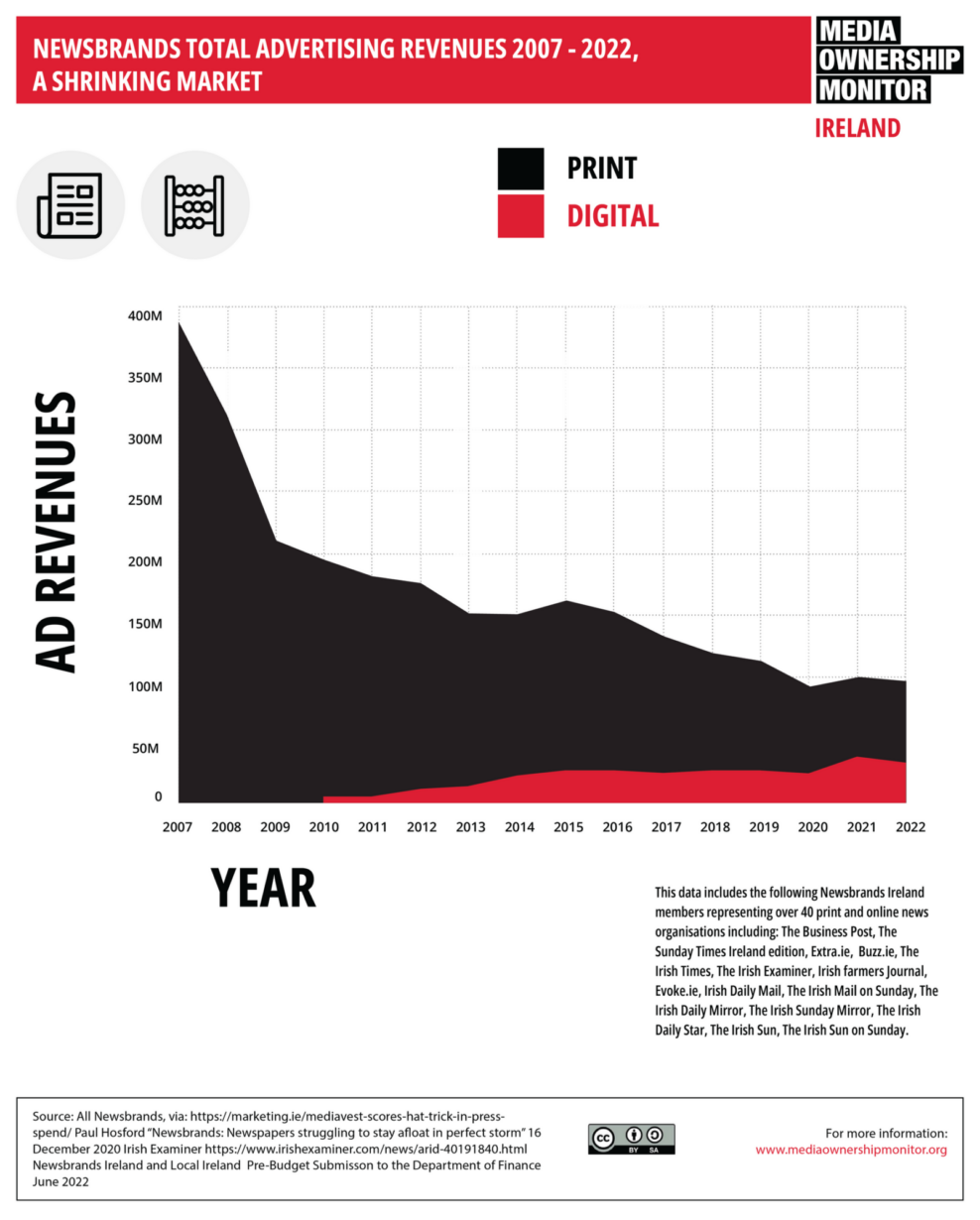

Molann PWC gurbh fhiú €4.9bn an earnáil Siamsaíochta agus Meán in Éirinn ina hiomláine in 2021. Maidir le nuachtáin, measann PWC gur thit an t-ioncam iomlán ó €507m in 2018 go €408m in 2021. Ag féachaint thar thréimhse níos faide, léiríonn figiúirí an Bhiúró Iniúchóireachta Cúrsaíochta do nuachtáin náisiúnta maidine agus tráthnóna titim ó 800,000 in aghaidh an lae in 2007 go dtí 351,000 in 2018 (ina dhiaidh sin tharraing an chuid is mó de na mórtheidil siar as an gcóras ABC). Agus, cé gur chóir a bheith faichilleach leis na figiúirí seo, tugann figiúirí caiteachais fógraíochta de chuid Institiúid Chleachtóirí Fógraíochta na hÉireann (IAPI) agus figiúirí caiteachais fógraíochta Nielsen le fios go bhfuil ioncam iomlán fógraíochta nuachtáin tite ó bheagnach os cionn €1bn in 2007 go €159m in 2021.

Molann PWC gurbh fhiú €227m an earnáil fógraíochta teilifíse in 2021 agus gurbh fhiú €532m an margadh síntiúis teilifíse (agus formhór an mhargaidh ag Sky agus Virgin Media) (mheas an IAPI gur shroich luach iomlán na fógraíochta teilifíse buaicphointe de €416m in 2008). Go sonrach, amhail 2021, is cosúil go sáraíonn ioncam iomlán na seirbhísí sruthaithe (€244m) caiteachas fógraíochta.

As na hearnálacha oidhreachta ar fad, tá an raidió ag téarnamh níos mó ná earnáil ar bith eile. Cé go rianaíonn figiúirí an IAPI laghdú i gcaiteachas iomlán fógraíochta raidió ó €150m in 2008 go €73m faoi 2014, tháinig téarnamh ar an earnáil ina dhiaidh sin agus figiúirí Nielsen ag tabhairt le fios gur shroich caiteachas ar fhógraíocht raidió €162m in 2021. Níl meastacháin ó fhoinsí eile chomh dearfach, ach fós féin léiríonn siad roinnt fáis san earnáil.

Is iad na meáin ar líne is mó a bhain tairbhe as aon fhás atá tagtha ar earnáil fógraíochta na hÉireann. Bunaithe ar thaighde PWC a choimisiúnaigh IAB Ireland, b'ionann luach iomlán an mhargaidh fógraíochta idirlín in 2009 agus €97m. Tugann an fhoinse chéanna le fios gur shroich an caiteachas iomlán fógraíochta ar líne €830m in 2021. Cé go léiríonn figiúirí ó CORE luach na fógraíochta ar líne beagán níos ísle (ag €789m) measann siad fós gurb ionann caiteachas fógraíochta ar líne agus beagnach 60% den chaiteachas fógraíochta ar fad in Éirinn. (Tá meastachán níos ísle fós á thairiscint ag PWC maidir le fógraíocht ar líne: €660m do 2021.)

Online vs. Legacy

The contrasting financial fortunes of legacy and online media Ireland since 2008 have given rise to a narrative of a causal link between the decline of one sector and the rise of the other. In particular, Legacy media have complained that online media have undermined the long-established advertising-for-news quid pro quo. Thus those media outlets which performed a public service by performing news gathering and dissemination services have seen their commercial income dwindle whilst online platforms (with little-to-no news production facilities) of their own have thrived. Legacy media organisations have also chafed at the fact that they are subject to content regulation which online media – albeit in a pre-Digital Services Act eta – have largely evaded. There have been calls, amplified through submissions to the Irish Future of Media Commission in 2020 and 2021, to use the levy on digital intermediaries provided for in the most recent iteration of the European Union’s Audiovisual Media Services Directive, to cross-subsidise the activities of traditional news media from the profits of their online counterparts.

The Irish Economy - Rich on paper

Ireland is considered to be a prosperous country by international standards. Measured by Gross Domestic Product (GDP) per capita, it is the second richest country in the world as of 2023, only behind Luxembourg. As of mid-2023, the unemployment rate was 4.1% which is effectively regarded as full employment. Public debt is less positive: per capita debt stood at €44,000 per person as of the end of 2022, one of the highest per capita debt burdens in the world. In any case a reliance on conventional economic measures such as GDP hugely overstates the actual wealth of the country.

Irish GDP is artificially inflated by the presence and activities of multinational companies from the information and communications technology, pharmaceutical and medical technology sectors. The impact of these players on the small economy is significant: as of 2022, the Irish revenues of just three - Apple, Alphabet and Meta – are worth more than half total national GDP. Depreciation on the capital assets (including Intellectual Property) owned by multinationals is included in Irish GDP. Furthermore, Ireland’s low rate of corporation tax creates a strong incentive for multinationals to establish headquarter operations in Ireland despite conducting relatively little economic activity in this country. As a consequence the undistributed profits of these multinationals are also attributed to their Irish operations further inflating Irish GDP.

An alternate measure of the scale of the economy, Gross National Income (GNI), which strips out some of these distortions, offers a more accurate picture of the Irish economy. In most countries, GDP and GNI are roughly equivalent. In Ireland, however, GNI is about 40% lower than GDP and Ireland ranks 8th (not 2nd) in the EU on the basis of GNI per capita.

Other potential indicators rank Ireland even lower. Using “Actual Individual Consumption”, based on consumption by households and consumption spending by government on individual services, Ireland was ranked 12th in the EU in 2019. Even this does not reflect the impact of the high cost of living: by 2019 Irish prices were approximately 25% higher than the Euro area average.

“The Value and Future of Public Service Media”, EBU (2020), Appendix 2, page 5.